The introduction of Open Banking gives clients of European banks unprecedented control over their own data and its use for economic purposes. Customers can determine with whom they want to share their financial data and thus also use it to their own advantage. But what is so revolutionary about providing personal bank data?

What does Open Banking mean?

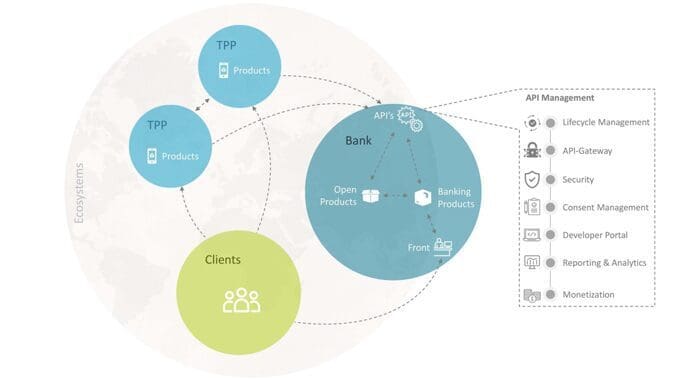

Current technologies enable collaboration between traditional banks and other providers, e.g., Fintechs, through the exchange of information and data via APIs (application programming interfaces). The term API has its origin in the software sector and refers to an interface that enables the transfer of data and communication between originally separate systems. In the financial industry, development in Europe was accelerated by the introduction of the Revised Payment Services Directive (PSD2) in 2016. The regulatory framework requires European banks to disclose APIs and make them accessible to other service providers. The aim of this requirementab is to strengthen competition and the user experience. In Switzerland, this goal is being driven forward by various interest groups, with the most prominent example being the central platform model, b.Link SIX. Here, third-party providers and banks are covered simultaneously with a single connection. The standardization of API specifications and contracts stands out as an advantage.

Current technologies enable collaboration between traditional banks and other providers, e.g., Fintechs, through the exchange of information and data via APIs (application programming interfaces). The term API has its origin in the software sector and refers to an interface that enables the transfer of data and communication between originally separate systems. In the financial industry, development in Europe was accelerated by the introduction of the Revised Payment Services Directive (PSD2) in 2016. The regulatory framework requires European banks to disclose APIs and make them accessible to other service providers. The aim of this requirementab is to strengthen competition and the user experience. In Switzerland, this goal is being driven forward by various interest groups, with the most prominent example being the central platform model, b.Link SIX. Here, third-party providers and banks are covered simultaneously with a single connection. The standardization of API specifications and contracts stands out as an advantage. “Data is the new oil,” as the Economist aptly described it in 2017. That customer data does not belong to the banks, but to their customers, is a fundamental premise that now prevails and could uproot the finance landscape enormously.

Open Banking has the potential to provide enormous added value for customers if the necessary foundations have been laid. As long as these have not yet solidified, it will probably be a while before a sharp increase in innovations in this area can be expected.

Simplified access for third-party providers enables data-driven innovation. Companies in the real estate market serve as an example. By analyzing vast amounts of data, platforms can help customers find the perfect new home based on the user’s payment habits. Preferences, such as where a customer shops on a weekly basis, could help to find a suitable apartment, e.g., near that store. Data based on financial behavior allows providers to identify the lifestyle and expectation of customers and to monetize these insights. It is possible to derive a variety of assumptions from the correct categorization of a customer. Has the customer taken out a student loan? Is the customer repaying a mortgage? Answering such questions allows predictions that, e.g., the student will look for lower-cost solutions. Data extraction from Open Banking APIs allows marketers to approach their customers even more specifically and increase their conversion rate through more relevant advertisements. In this sense, we can safely regard the databases of financial service providers as oil fields, and tapping these fields can be economically enormously profitable.