2026 IT Sourcing Study – Netherlands

The 2026 Dutch IT Sourcing Study, conducted in collaboration with Whitelane, is the most comprehensive assessment of IT service and cloud platform providers in the Netherlands. Based on input from more than 350 of the country’s largest IT-spending organisations, the study evaluates nearly 800 unique IT sourcing relationships and over 1,150 cloud platform relationships.

Insourcing trend continues to rise.

Just over a third of organisations (36%) plan to increase spending on external IT providers over the next two years, while 29% expect their spending to remain stable. Meanwhile, 26% intend to reduce external IT expenditure, up from 20% in 2025.

Most of these organisations plan to bring previously outsourced work in-house, continuing an insourcing trend that has been growing since 2023.

Public sector drives external IT services growth.

51% of public sector respondents plan to increase spending on external IT providers, 15 percentage points above the overall average, and only 15% expect to spend less. In contrast, manufacturing and chemicals remain cautious, with just 15% planning to increase external IT spending and 35% expecting reductions.

Flexibility and innovation drive increased outsourcing.

Scalability is the leading driver for increased use of external IT providers, cited by 53% of respondents. Access to emerging technologies comes in second at 49%, while 46% highlight the ability to focus on core business activities.

Knowledge retention and cost efficiency drive insourcing plans.

Organisations reduce reliance on external providers primarily to retain critical knowledge internally (59%). Nearly half of clients (49%) consider insourcing more cost-effective than outsourcing, and 29% plan to increase workloads within captive delivery centres.

Nearshore outsourcing shows the strongest growth potential.

Thirty-six percent of organisations plan to increase their use of nearshore delivery, compared with just 9% planning to reduce it. Offshore delivery is also expected to grow (+29%), while onshore outsourcing continues to decline, with 35% of organisations planning reductions. Nearshoring remains attractive because it combines cost efficiency with regulatory alignment, lower risk, and cultural proximity.

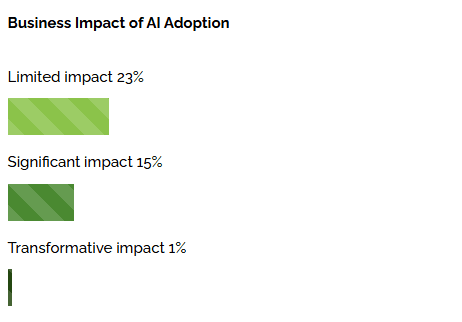

AI adoption is now mainstream, but its impact remains limited.

AI and GenAI adoption are nearly universal: only 2% of respondents report no use. Widely available tools such as ChatGPT and Microsoft Copilot are used by 38% of organisations, while 20% experiment with internally developed AI solutions.

Although 15% now report significant business impact from their own AI initiatives (up from 2% last year), truly transformative impact remains rare at just 1%.

Captive IT delivery centres remain selective; nearshore is the most popular option.

Most organisations (53%) do not operate a captive IT delivery centre. Among those that do, nearshore models dominate: 12% operate a nearshore-only captive, 4% an offshore-only model, and 17% a hybrid setup.

Key benefits cited by clients include cost savings (53%), improved knowledge retention (50%), and higher service quality (44%).

Sovereign IT is increasingly important, particularly in the public sector.

37% of organisations report that sovereign IT has a medium to large impact on their IT strategy. The impact is strongest in the public sector, where 62% cite significant impact due to regulatory requirements, data sensitivity, and public accountability. In manufacturing and chemicals, only 21% report a similar influence.

Sovereignty concerns are reshaping cloud strategies.

Overall, 26% of companies plan to reduce their reliance on hyperscalers due to sovereign IT concerns. This trend is strongest in the public sector, where 45% plan reductions. In financial services, the reduction is also significant, with 25% of organisations indicating that they will reduce their public cloud load.

While these repatriations from public to private cloud are real, overall public cloud adoption will continue to rise, albeit at a slower pace than anticipated some years ago.

Service provider landscape becomes more competitive.

The general satisfaction ranking includes 43 IT service providers, the highest number to date. This year’s ranking introduces five new entrants: Hexaware, ilionx, KPMG, PwC and Thales. Levi9 and Schuberg Philis share first place (89%), followed by EPAM (87%), TCS (82%), and CGI (81%). The average satisfaction across all providers is 75%.

Clients highlight the lack of challenge from their providers.

A lack of challenge from service providers is the most commonly cited weakness, identified by 45% of respondents. Insufficient business understanding follows at 30%, while 25% say providers fail to act as true partners.

AWS and Microsoft Office 365 top cloud rankings.

Amazon Web Services (AWS) leads the infrastructure cloud platforms ranking with 77%, while Microsoft Office 365 ranks first among software cloud platforms (78%). Overall satisfaction has improved in both the infrastructure and software cloud rankings, increasing by three and four percentage points, respectively.

Please note: the full report is available in English.